This post was taken from Distressed Investing’s website.

AMR: EETC Recovery 11/29/11

This morning, AMR Corporation (“AMR”), and its subsidiary American Airlines, Inc. filed for bankruptcy protection in the Southern District of New York.

To say that this was a surprise to the market would be a bit of an understatement. To give you a sense of how far out of left field the timing of the bankruptcy filing was, the December 2011 CDS traded yesterday at 5.5 – 8.5 points up front. It closed today at 83 points up front. If you polled the majority of sell side analysts out there, they would have told you that AMR had the liquidity to survive at least until mid-2012 and possibly beyond.

Here is an example. AMR has over $3 billion dollars in municipal debt. Each of these securities could be unsecured or secured by leases on gates or owned maintenance facilities. A good friend pointed out that CUSIP 01852LAB6, an Alliance Texas Airport Authority Bond, with ~$125M outstanding was due to be paid this coming Thursday. It’s unsecured. Pain.

As of now, I will be completely honest and point out that the majority of my time over the past few months (since the AMR bankruptcy scare in October), has been on the EETC side. I will end the post with some overall thoughts on the controversial 7.5% notes secured by international routes and some questions on the general unsecured pool. But for now, let’s dig into EETC securities.

EETCs (Enhanced Equipment Trust Certificate) are secured securities backed by the financing of individual airplanes. When an airline or lessor like ILFC purchases a plane from Boeing or Airbus, they finance the purchase. They do this on a number of planes. These financings, from the pool of purchased planes, are then packaged equipment notes, pooled, and then placed into a EETC structure and sold to institutional investors. These securities are classified as pass through securities because as each individual equipment note backed by an airplane financing pays interest and principal payments, these payments are passed through to the overarching EETC to pay interest and amortization payments.

Depending on the individual structure, EETC are tranched into A, B, and C tranches. The A’s will be the senior piece of paper and will recover first in a bankruptcy / default scenario (cross-subordination). With that said, the A tranches will almost always have the longest weighted average life as amortization payments of the EETC go to pay the C, then the B off first. Loan to values scale with the tranches, so an A tranche may be marketed at 60%, a B tranche at 75%, and a C tranche at 90%. Because of this, as well as the contractual seniority, A’s come with a lower coupon despite the longer tenor. A G tranche in EETC land refers to a EETC tranche wrapped by the likes of Ambac or MBIA.

A final quick note, on amortization: all amortization and principal pay downs are not created equal. There are instances when a EETC structure will contain a lot of great planes, but also a lot of terrible planes. An investor should recognize that each underlying financing references an individual aircraft. Those financings have different maturities and the LTV of a EETC structure can change dramatically if those equipment notes backing good planes mature first (i.e. you are in a stub of bad equipment notes.

Each EETC is different, and newer vintage EETC have protective benefit to lenders in the form of cross default and cross collateralization. If AMR defaults on one equipment note backing an airplane in a EETC, the cross default means ALL equipment notes are triggered in that same EETC. Cross collateralization means that deficiencies in one equipment note can be offset by gains in another equipment note. These concepts are very important to the AMR bankruptcy as the 2009-1, 2011-1, and the 2011-2 EETC structures feature both cross default and cross collateralization provisions.

Another unique characteristic of the EETC structure is referred to in the market as a “liquidity facility.” These facilities, backed by highly rated banks, provide for the payment of interest on the various tranches of the EETC for 18 months. This allows creditors that have taken ownership of rejected planes time to refurbish, provide maintenance for, and re-market (sell) planes with the intended purpose to avoid distressed, under-the-gun sales.

Finally, and topical, as AMR has filed for bankruptcy are the concepts of 1110 (a), 1110 (b), and 1110 (c). Under 1110(a), aircraft have their own place in bankruptcy law in that debtholders can take back the aircraft 60 days after a bankruptcy filing if airline does not cure the default (i.e. pay interest and amortization on the note). This is where the concept of affirm or reject comes in to play and where investors can start differentiating themselves in terms of the knowledge they bring to a particular bankrupt airline’s situation. The aforementioned 1110 (b) can be thought of as a renegotiation between the airline and the pass through note holders (and involves adequate protection payments for use of plane). And 1110 (c), or a rejection, is when a plane is returned to the lender.

There are more nuances to the structure (purchase option for subordinate tranches, adjusted expected distributions, CODI claims, etc), but for now, this will do, and as AMR exercise their right to accept or reject collateral in various structure, we can flesh out the details. In its letter to aircraft creditors, AMR said this:

We cannot afford to retain all the aircraft currently in the American and American Eagle fleets at their current rates, and so we have no choice but to make substantial reductions in the cost of the aircraft which we retain. Moreover, in view of the large number of aircraft we have on order from Airbus and Boeing, we also seek to accelerate our fleet renewal strategy and, as a result, we do not require the use of all aircraft currently in our fleets. Additionally, to conserve our liquidity, subject to the requirements of the U.S. Bankruptcy Code, during the 60-day Section 1110 period, we plan to make payments when due of aircraft rent and mortgage principal and interest payments only on certain aircraft in our fleets.

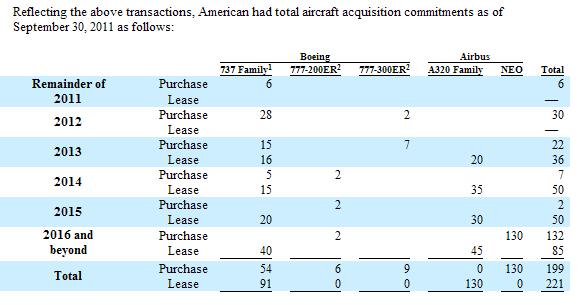

To put it lightly, AMR, out of all the domestic carriers, has an extensive order book. Here is the disclosure from the most recent 10Q

- Reject old, fuel inefficient airplanes (MD 80s) that will be replaced by the 737-800 family (not all will be rejected, but most will)

- Renegotiate every labor contract out there to make yourself more cost competitive with the industry. In fact, AMR actually put in a graph in the aforementioned affidavit displaying how weak their margins are to competitors

- Rationalize your network in terms of routes and gates (i.e. leave Chicago for instance). This may require asset sales in addition to flat out defaulting on municipal debt.

- Reject the pension and put it to the PBGC

The question then for investors becomes: Where can I get the best bang for my buck? In EETC land, the question of reject or accept under 1110 becomes paramount. For instance, the 6.977% notes are the 2001-A vintage. They are trading in the mid 50s. There is $177M bonds outstanding. Backing those bonds are 32 MD-83s delivered in the last 90s. To figure what this EETC tranche is worth, you need to take a number of things into consideration:

- Will they accept or reject these planes? Maybe they accept a few and continue paying interest on the underlying equipment notes and reject all the rest. As every one of these MD 83s are owned by Boeing, it is more likely they reject than accept (airlines, for various tax reasons, are somewhat reluctant to reject planes they own). But if you believe they will accept a lot of this collateral, you would be more bullish all else being equal

- If they do reject planes, how much are those planes worth after they pass maintenance tests and monies are spent for re-marketing (you could also melt the planes for steel value)

- If the amount of debt is not covered by the asset sale process, you would have a general unsecured claim to the AMR estate. You then need to figure out how much that claim is worth and add that to your recovery.

- A smaller, but important consideration: Interest will be paid on this EETC for 18 months via the liquidity facility. This paid interest becomes a super senior claim over your A-tranche (i.e. if the liquidity facility provider pays out $100 dollars in payments, $100 dollars of debt is now ahead of you in the waterfall). This can be important in very low dollar price bonds as you are creating a very cheap option after deducting the present value of interest payment

Determining if a plane will be rejected or accepted is more of an art of science. Many, many factors come into play here include (but not limited to):

- Type of structure the equipment note backing the plane is a part of. For instance, an airline may be less likely to reject a plane backed by an equipment note in a EETC that has cross default provisions, all they could lose all planes in that structure

- The important of the plane in relation to the overall fleet and future fleet build out plans. As noted above, AMR is purchasing a significant number of 737-800s, meaning they are less likely to reject these planes.

- The unique aspects of a plane in terms of its range and capacity. If an airline used to have significant need for wide-body planes, and now doesn’t because of route / slot / gate changes, they may be more likely to reject those planes

- The maintenance schedule of a particular plane may be onerous in the coming years and be a cash flow drain on the airline which means its more likely to be rejected

- Cost of financing the underlying equipment note versus market rate. This can be extended to the overall EETC structure – i.e. could AMR go out in the market today and get a better deal for some of their high coupon EETC structures?

The value of a plane in a re marketing exercise is really a function of supply and demand. One thing I look for are planes that many different airlines use. Some planes only fit 3-4 carriers making them harder to sell into the broader market place. Demand for 737-800 is quite high and queue times for delivery is 5-6 years out, meaning these planes would easily be remarketed. There are a number of appraisal companies out there that will tell you what they think each and every kind of aircraft out there is worth today, next year, and 5-10 years out. As a rule of thumb, I lop of 15-25% off the top on these appraisals for a sanity check.

With all that said, that is how you approach AMR’s EETC structures. I definitely think some are interesting and are high current yielding pieces of paper.

Over the next few weeks, I will be spending time digging through and laying out every piece of paper that I can find to ascertain market opportunities. As noted above, there is A LOT to work through, and one analyst could spend an entire year or three just understanding each underlying municipal, EETC, Pass Through, Secured, etc piece of paper. With that, I’ll end the post with a few questions that linger in my mind that I will try to tackle over the next week (and if you have any thoughts, please feel free to email me to discuss)

- What is exactly the pension underfunded status and how large an unsecured claim will the PBGC put to the estate? What effects do recent changes to pension legislation as it pertains to airlines have on this number?

- If the liens backing the 7.5% were not perfected, do the unsecured’s make a case that they should see benefits from that collateral? What really is the value of that collateral? $20M per slot pair according to Air Canada’s recent valuation for Heathrow. But what about Japanese, where AMR is weak, and China routes?

- The 13% Notes, while not a traditional EETC structure, kind of scare me. Does it make sense to reject slightly older 737-800s to restructure a small, but very high cost piece of paper? The 10.5% Notes are a slightly different story – and with such a large contingent of 757-200s in the structure, which AMR has admitted they are rationalizing next year, are equally frightening

- Who is going to own the equity in this thing when all is said and done? A hodge podge of unsecured creditors including the PBGC? How does this affect the NOL, which I believe is around $8 billion dollars.

And these are really just structural questions. The big question on everyone’s mind is: After all is said and done, what kind of EBITDA margins are we talking here? Is it 5%? 7%? Given the size of the revenue line here a 100 basis point move in margins is massive when you capitalize it a 4-5x.

This is going to be a fun one. I can definitely say that I have more than enough to be working on in distressed debt land with the recent filings of AMR, DYN, PMI, and MF, along with a number of legacy situations. Great time to be involved in distressed debt investing.