Distressed Debt Investing Website 12/20/10

As noted many times on this site, Chapter 11 cases are expensive. From paying $700-$1200/hour for senior lawyers, success based fees for financial advisors, and (in my opinion the most important) business issues such as loss of customers, suppliers, employees, etc costs start to add up. That being said, and because of certain 2005 changes to the bankruptcy code regarding exclusivity timing, more and more bankruptcies are going the prepack bankruptcy route. And to make sure things go smoothly, the creditors driving the show are offering a gift to possible dissenting classes to make sure the Chapter 11 proceedings go off without a hitch.

Last week, after all the hub bub of the Great Atlantic’s bankruptcy filing, people seem to have forgotten that Insight Health filed for bankruptcy just a few days earlier. Here is the press release:

InSight Health Services Holdings Corp. (“Insight Imaging” or “the Company”) (OTCBB:ISGT.ob – News) today announced it had reached an agreement in principle with holders of a significant majority in aggregate principal amount of its outstanding senior secured floating rate notes due 2011 (the “Notes”) regarding a restructuring of the Notes. Insight Imaging has entered into a restructuring support agreement (the “Support Agreement”) with such holders (the “Supporting Holders”), which contemplates restructuring the Notes through a jointly agreed plan of reorganization to be filed with the bankruptcy court (the “Court”). The terms of such pre-packaged plan are set forth in a term sheet made part of the Support Agreement, but may be amended or modified in accordance with the terms of the Support Agreement (a “Qualified Plan”). The terms of the Qualified Plan contemplate an exchange of all of the Notes for all of the common stock of the reorganized Company upon exit from bankruptcy, resulting in the elimination of 100% of the Notes from the Company’s balance sheet.

The Support Agreement provides that the Supporting Holders will, among other things, vote to accept a Qualified Plan and support a debtor-in-possession financing facility (the “DIP Facility”). The Company is currently in discussions with Bank of America, N.A. (“Bank of America”), the administrative agent under its current revolving credit facility, regarding the DIP Facility. The Support Agreement will require Insight Imaging and certain of its subsidiaries to file a Qualified Plan with the Court, obtain a confirmation order from the Court and effectuate the Qualified Plan within the time-frames set forth in the Support Agreement.

Insight Imaging also announced that holders of greater than 75% of the principal amount outstanding of the Notes, the trustee under the indenture governing the Notes and the collateral agent under the security documents relating to the Notes have entered into an agreement to forbear from exercising their remedies under the Notes, the indenture and related security documents as a result of events of default arising from the November 1, 2010 interest nonpayment and the expiration of the applicable 30-day grace period. The forbearance period ends not earlier than December 10, 2010, by which time the Company expects to have filed a prepackaged plan of reorganization. Bank of America has also extended the forbearance period under the Company’s revolving credit facility, as amended, from December 1, 2010 to December 15, 2010.

Kip Hallman, Insight Imaging’s President and CEO, stated, “This restructuring is being undertaken to eliminate more than $290 million of debt, substantially improving our cash and liquidity position. We intend to complete the reorganization as quickly as possible. In the meantime, we will continue to operate our business as usual to provide quality services to our customers and our patients. We look forward to emerging as a much stronger business, with a capital structure that will enable us to maximize the long-term value of the company.”

For those interested, you can find the Insight Health bankruptcy docket here: Insight’s Chapter 11 docket

As those in the distressed community will know, this will not be the first trip to the rodeo for Insight. From the disclosure statement:

On May 29, 2007, InSight Health Services Holdings Corp. and InSight Health Services Corp. Filed voluntary petitions to reorganize their business under Chapter 11 of the Bankruptcy Code in the U.S. Bankruptcy Court for the District of Delaware (Case No. 07-10700) (the “2007 Reorganization”). The filing was in connection with a prepackaged plan of reorganization and related exchange offer. On July 10, 2007, the Delaware bankruptcy court confirmed InSight Health Services Holdings Corp. and InSight Health Services Corp.’s Second Amended Joint Plan of Reorganization pursuant to Chapter 11 of the Bankruptcy Code. The plan of reorganization became effective and InSight Health Services Holdings Corp. and InSight Health Services Corp. emerged from bankruptcy protection on August 1, 2007. Pursuant to the confirmed plan of reorganization and the related exchange offer, (1) all of InSight Health Services Holdings Corp.’s then existing common stock, all options for the common stock and all of InSight Health Services Corp.’s 9.875% senior subordinated notes due 2011, or senior subordinated notes, were cancelled and (2) Holders of InSight Health Services Corp.’s senior subordinated notes and Holders of InSight Health Services Holdings Corp.’s common stock prior to the effective date received 7,780,000 and 864,444 shares of newly issued common stock, respectively, in each case after giving effect to a one for 6.326392 reverse stock split of such InSight Health Services Holdings Corp.’s common stock.

While the reorganization attempted to deleverage InSight Health Services Holdings Corp.’s and InSight Health Services Corp.’s balance sheets and improve their projected cash flow after debt service, both still have a substantial amount of debt, which requires significant interest payments. As of September 30, 2010, the Debtors had total indebtedness of approximately $298.3 million in aggregate principal amount, including InSight Health Services Corp.’s $293.5 million in principal amount of Senior Secured Notes.

Looks like we have ourselves a good ole’ Chapter 22 on our hands.

Who are the parties of interest here? Well we know a Plan Support agreement will have been filed in a pre-pack like this, so let’s take a look at the disclosure statement and see what we can find. On page 494 – 496 of the PDF, one can see that J.P. Morgan’s Credit Trading Group and affiliates of Black Diamond have signed the agreement. To give you a sense of how this bond has traded over the past few years, take a peak:

According to Trace (the graph above is based on Trace versus my message runs) there was a million + dollar worth of bonds traded on the 22nd of November. Alex Bea, a fantastic distressed debt trader from JPM who was the axe in this name, stoppped making markets sometime in October – thinking they got restricted and all that was left was sporadic runs from a number of brokers / dealers.

For the rest of this post, I will assume the bonds trade at 25 cents on the dollar. The allowed claim, according to the plan, of the Insight secured floaters is $293.5M with very little debt ahead of you in the capital structure. There has been a $15M DIP authorized which, according to the disclosure statement, will be rolled into a $20M revolving exit facility.

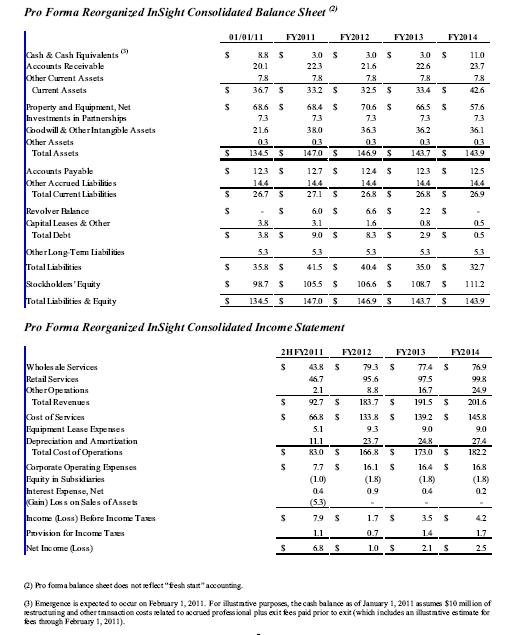

The disclosure statement also came with projections:

As you can see, the company plans to emerge with very little debt and a marginal cash balance. What does that mean for our bonds?

Insight Health has two direct publicly traded comps: Alliance Healthcare Services (AIQ) and Radnet (RDNT). Both stocks have had lackluster performance in the face of declining reimbursement rates in a predominantly fixed cost structure combined with hefty debt loads. According to Bloomberg, RDNT trades at 5.1x 2011 EBITDA and AIQ trades at 4.9x EBITDA. What does that mean for Insights bonds?

According to the projections, Insight looks to generate approximately $25M of EBITDA in 2012 (full year 2011 not really helpful given reorg costs). At 5.0x, this translates into $125M of value versus $293.5M of claims or 40 cents on the dollar – which at a purchase price of 25 gives us approximately a 25% IRR over 2 years. Not too shabby. Of course, if we haircut the multiple 1.0x turns reflecting the weaker mobile business of Insight, we get an IRR closer to 16%.

As we’ve talked about in previous posts, one really has to scrutinize projections. Why? Because management’s incentive is to create a low valuation for the stock so their upside is greater. In Insight’s case:

The Management Equity Plan will provide for a certain percentage of New Common Stock, not to exceed eight percent (8%) of the fully diluted New Common Stock, to be reserved for issuance as options, equity or equity-based grants in connection with the Reorganized Debtors’ management equity incentive program and/or director equity incentive program. The amount of New Common Stock, if any, to be issued pursuant to the Management Equity Plan, and the terms thereof shall be determined by the New Board on or as soon as reasonably practicable after the Effective Date.

The scrutiny of projections will be for another post. The question I am trying to address: If the floaters are going to make 16-25% in possibly artificially low projections and management is making off with possibly 8% of the company, what is happening to the equity? The equity is receiving a “gift”.

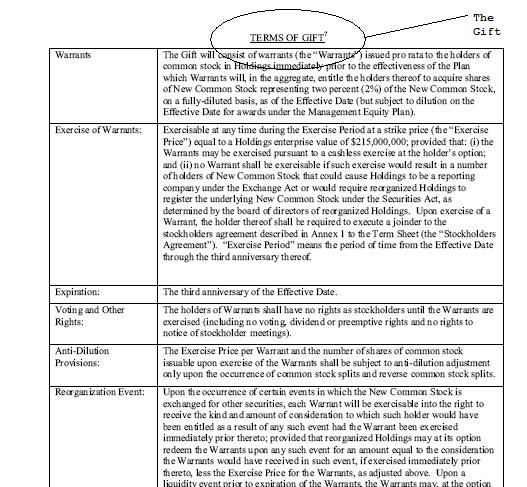

You think I am using that term as slang. No, gentle reader, it really is called a a “gift”:

Now what are the specifics of this gift:

- They are warrants to buy up to 2% of stock on a fully diluted basis

- Three year expiration

- Exercisable when enterprise value is greater than $215M

Exercisable when EV is greater than $215M? In 3 years?? $215M on the contemplated $25M of EBITDA is an 8.6x multiple. Or backing into the cash flow required on a more realistic 5.0x multiple, EBITDA would have to grow 20% a year for the next three years to reach $43M for these warrants to be in the money. In my opinion, highly doubtful.